Cost of Living in Florida 2026: What You'll Actually Spend

Luana B. Gann, Editor

6/5/2026

Let's be real with each other for a second.

You've probably Googled "cost of living in Florida" and landed on articles that told you Florida is gloriously cheap — the land of tax-free sunshine where your dollar stretches like saltwater taffy. Then you've probably also read the scary headlines: Florida insurance crisis! Rent through the roof! Hidden costs everywhere!

On this page:

Housing in Florida 2026

Healthcare Costs in Florida

Florida vs Other States

Sample Monthly Budgets

Smart Ways to Stretch Your Florida Dollar

The truth, as usual, lives somewhere in the middle. And that's exactly where we're going to meet you.

Florida can be an outstanding financial move. The tax savings alone — especially if you're coming from a high-tax state like New York, California, or Illinois — can put thousands of dollars back in your pocket every single year. But there are real costs that catch newcomers off guard: homeowners insurance, the summer electric bill, and what we'll politely call the Great Florida Auto Insurance Surprise.

We're going to walk through it all. Real numbers. Real breakdowns. City comparisons. And at the end, you'll have a clear picture of what your Florida life will actually cost — not what a billboard promised you.

What Does It Cost to Live in Florida in 2026?

The Big Picture

Florida's overall cost of living sits at approximately 2–5% below the national average when you factor in no state income tax. But that headline number can be misleading, because Florida is not one uniform market — it's about 67 counties' worth of wildly different real estate prices, insurance zones, and local economies all wearing the same "Sunshine State" name tag.

A studio apartment in Miami Beach and a three-bedroom house in Ocala are both "Florida." The difference in monthly cost? Potentially $2,000 or more.

Here's what we'll break down:

🏠 Housing (rent and buy)

⚡ Utilities

🛒 Groceries and dining

🚗 Transportation and auto insurance

🏡 Homeowners insurance

🏥 Healthcare

🎉 Lifestyle costs

💰 Tax advantages (and how to actually calculate yours)

📊 City-by-city comparison

🧾 Sample monthly budgets

Let's dig in.

🏠 Housing in Florida 2026

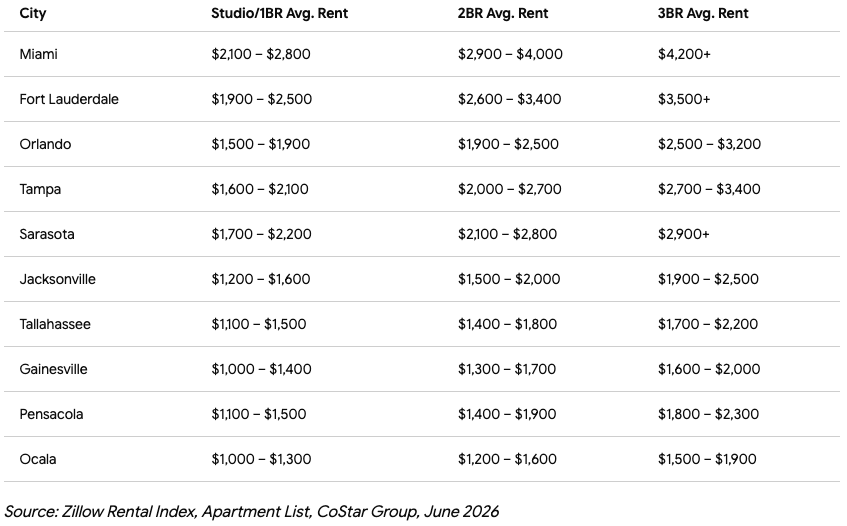

Renting in Florida

Rents surged dramatically between 2020 and 2023, and while the pace has slowed, they haven't come back down. As of mid-2026, Florida renters are looking at:

Florida Current Take: If you're relocating and flexibility is your friend, look seriously at Jacksonville, Tallahassee, Ocala, or the Pensacola area. You can rent a genuinely nice place for what you'd pay for a closet in South Florida. That's not an exaggeration. We've seen it.

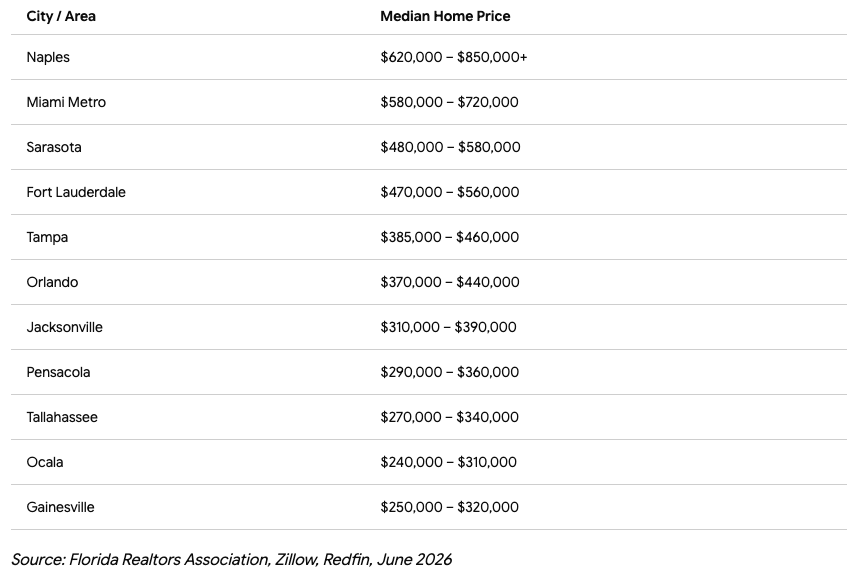

Buying a Home in Florida

The Florida housing market remains competitive, particularly in coastal and metro markets. Here's where median home sale prices sit in 2026:

Florida's Homestead Exemption — Your Built-In Discount

If you purchase a home and make it your primary Florida residence, you're entitled to the Homestead Exemption — which reduces your property's assessed taxable value by up to $50,000. That translates to roughly $750–$1,500 in annual property tax savings depending on your county's millage rate.

Even better: Save Our Homes caps annual increases on your home's assessed value at 3% or the rate of inflation (whichever is lower), protecting you from runaway reassessments if the market heats up around you.

Critical deadline: You must file for your Homestead Exemption by March 1 of the tax year you're claiming it. Miss that date and you wait another year. Don't miss it.

🔗 See also: The Florida New Resident Checklist: 25 Things to Do After the Moving Truck Leaves — for a complete Homestead Exemption how-to

⚡ Utilities in Florida

Electric Bills: The Florida Reality Check

Here's the thing no one warns you about enough: your electric bill is going to be higher in Florida than almost anywhere you've lived before. Not slightly higher. Sometimes double.

Why? Because your air conditioner runs hard. Constantly. For roughly 8–9 months of the year.

Average Monthly Electric Bills in Florida (2026):

Household Size - Moderate Usage - Heavy AC Usage - With Electric Vehicle

Single/Studio

$95 – $130

$140 – $180

$160 – $220

2-Bedroom

$130 – $175

$175 – $240

$200 – $280

3-4 Bedroom

$175 – $250

$250 – $380

$290 – $430

Source: U.S. Energy Information Administration, Florida Public Service Commission, 2026

During peak summer months (July–September), it's not unusual for a family home's electric bill to spike $80–$150 above the monthly average. Set that budget aside now and you'll thank yourself later.

Pro tips for keeping your electric bill sane:

Set your thermostat to 78°F when home, 82°F when away (yes, really — your body adjusts)

Ceiling fans make a room feel 4–6 degrees cooler without dropping the thermostat

Check for Florida Power & Light, Duke Energy, or TECO energy-efficiency rebates — they're real and can cover parts of new AC units, smart thermostats, and insulation upgrades

Plant shade trees on the east and west sides of your home if you own

Water, Sewer, and Other Utilities

Utility - Average Monthly Cost

Electric

$130 – $250

Water & Sewer

$45 – $85

Natural Gas (if applicable)

$20 – $50

Internet (fiber or cable)

$60 – $100

Trash Collection

$25 – $45

Total Monthly Utility Average

$280 – $530

Good news: Most of Florida uses electric appliances rather than gas, so you may have one fewer utility bill than you're used to.

🛒 Groceries and Dining in Florida

What You'll Spend at the Store

Florida's grocery costs run approximately 3–5% below the national average — good news for your food budget. The Sunshine State's agricultural production means fresh produce, citrus, seafood, and tropical fruits are genuinely more affordable here than almost anywhere in the country.

Average Monthly Grocery Costs (2026):

Household Size - Budget Shopper - Average - Foodie/Organic

Single Adult

$250 – $320

$320 – $420

$450 – $600

Couple

$400 – $500

$500 – $650

$700 – $950

Family of Four

$650 – $800

$800 – $1,050

$1,100 – $1,500

Where Floridians shop to save: Publix (yes, it's beloved, and yes, the BOGO deals are legitimate financial strategy), Aldi, Costco, Walmart Supercenter, and Winn-Dixie. Publix is not the cheapest option — it's the nicest option. Your wallet may know the difference, but your soul might not care.

Dining Out in Florida

Florida's restaurant scene ranges from $2 local fish taco joints to $200-per-person tasting menus, so this category varies wildly by lifestyle. A reasonable mid-range dinner for two with drinks runs $60–$100 at a sit-down restaurant outside tourist zones.

If you're factoring dining out into your monthly budget, most Florida residents who eat out 2–3 times per week spend $200–$400/month per person on restaurants and takeout.

And yes — the occasional stop for fresh-caught grouper at a dockside shack is basically a mandatory Florida experience. Budget accordingly.

🚗 Transportation and Auto Insurance

Getting Around Florida

Florida is primarily a car-dependent state. Miami has a Metrorail and some bus service; Orlando has SunRail commuter rail and the I-Drive trolley; Tampa has HART bus service. But outside those metro cores, you're driving. Plan for it.

Average Monthly Transportation Costs:

Expense - Average Monthly Cost

Car payment (financed)

$350 – $750

Gas (average driver)

$150 – $220

Auto insurance (see below)

$195 – $290

Maintenance & registration

$50 – $80

Tolls (if applicable)

$30 – $120

Monthly Transportation Total

$875 – $1,460

Florida Auto Insurance: The Honest Conversation

We're going to level with you here, because Florida auto insurance is the thing that consistently surprises newcomers most.

Florida has some of the highest auto insurance rates in the nation. As of 2026, the average annual auto insurance premium in Florida is approximately $2,800–$3,600/year — compared to a national average of around $1,900/year.

Why? A combination of: high population density, heavy traffic, a high rate of uninsured drivers (Florida ranks among the top 5 states for uninsured motorists), frequent weather-related claims, and significant insurance fraud, particularly in the Miami-Dade area.

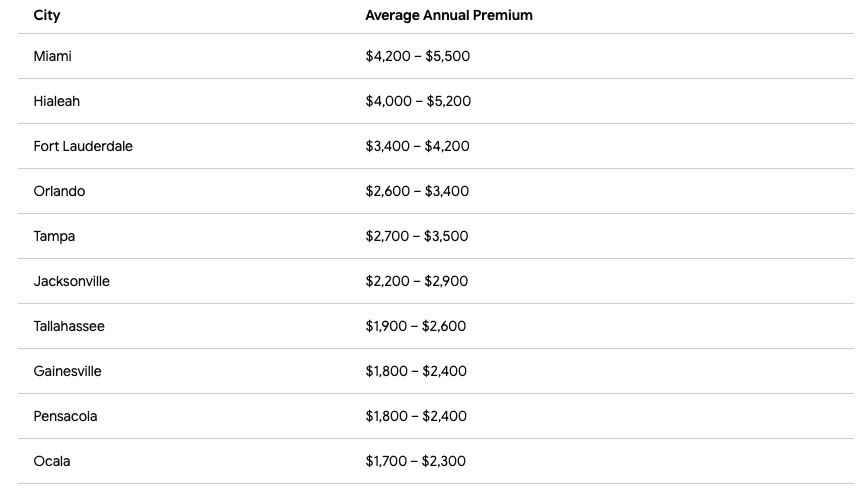

Average Annual Auto Insurance Rates by Florida City (2026):

Source: Bankrate, Insurify, Florida Office of Insurance Regulation, 2026

Ways to reduce your Florida auto insurance costs:

Bundle with your homeowners or renters policy (typically saves 10–15%)

Increase your deductibles if you have emergency savings

Maintain a clean driving record — Florida insurers weight this heavily

Ask about low-mileage discounts if you work from home

Shop every renewal — the market is competitive and rates vary widely by carrier in this state

Florida Minimum Coverage Requirements (2026): Florida requires $10,000 Personal Injury Protection (PIP) and $10,000 Property Damage Liability. Note: Florida does not require bodily injury liability — though most financial advisors strongly recommend carrying it.

🏡 Homeowners Insurance: Florida's Biggest Financial Wild Card

If there is one cost that genuinely distinguishes Florida from other states — and not in a fun way — it is homeowners insurance.

Florida's homeowners insurance market has experienced significant turbulence over the past several years. Multiple large private insurers left the state. Citizens Property Insurance Corporation (the state-backed insurer of last resort) expanded dramatically. Legislative reforms passed in 2022 and 2023 are working their way through the market, and conditions are gradually stabilizing — but premiums remain high by national standards.

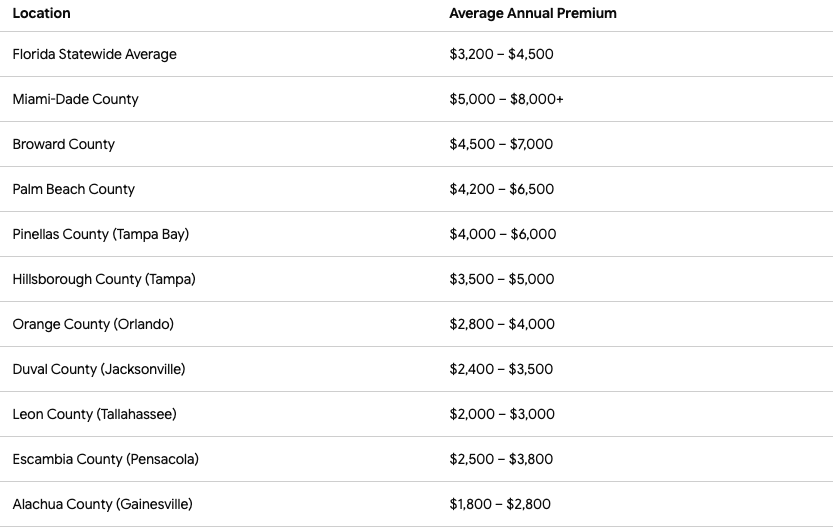

Average Annual Homeowners Insurance Premiums in Florida (2026):

Source: Florida Office of Insurance Regulation, Insurance Information Institute, 2026

Note: Coastal properties, older construction, and homes without hurricane-hardened features (impact windows, newer roofs) will pay significantly more. A new roof alone can reduce your premium by 25–40%.

What to Know Before You Buy

Wind mitigation inspection: Get one. It's typically $150–$200 and can reduce your premium significantly by documenting your home's hurricane-resistant features.

Citizens Property Insurance: If private market options are unavailable or unaffordable, Citizens provides coverage — but be aware that Citizens has been implementing rate increases and policies may be "depopulated" (transferred to private insurers) when market conditions allow.

Separate flood insurance: Standard homeowners policies do not cover flooding. Florida flood insurance is typically purchased through the National Flood Insurance Program (NFIP) and costs an average of $700–$2,500/year depending on flood zone designation. If you're near water, this is non-negotiable.

Homeowners insurance and flood insurance together represent one of the most significant financial differences between living in Florida vs. most other U.S. states. Factor them in before you fall in love with a house.

🔗 For more on what to do when you arrive in Florida: The Florida New Resident Checklist covers insurance timelines, registration deadlines, and what to set up first.

🏥 Healthcare Costs in Florida

Health Insurance

Florida's healthcare costs are close to the national average overall, though access and quality vary significantly by region. The state did not expand Medicaid under the ACA, which means some lower-income residents may find themselves in a coverage gap.

Average Monthly Health Insurance Premiums in Florida (2026):

Coverage Type - Average Monthly Premium

Individual (ACA Marketplace, mid-plan)

$380 – $520

Family of Four (ACA Marketplace, mid-plan)

$1,100 – $1,600

Employer-sponsored individual

$150 – $280 (employee share)

Employer-sponsored family

$450 – $850 (employee share)

Medicare Part B (65+)

$185/month (standard 2026)

Subsidies can significantly reduce ACA marketplace premiums for qualifying income levels. Use healthcare.gov's calculator for your specific situation.

Healthcare Costs at a Glance

ServiceTypical Out-of-Pocket Cost (no insurance)

Primary care visit

$150 – $300

Urgent care visit

$140 – $250

Emergency room visit

$1,000 – $3,500+

Prescription drugs (generic)

$10 – $40/month

Dental cleaning (uninsured)

$100 – $200

Florida has significant healthcare infrastructure — Mayo Clinic in Jacksonville, AdventHealth in Orlando, Cleveland Clinic locations in Weston, Moffitt Cancer Center in Tampa, and major academic medical centers in Gainesville and Miami. If healthcare access is a priority factor for you (especially retirees), Florida delivers strong options in metro areas.

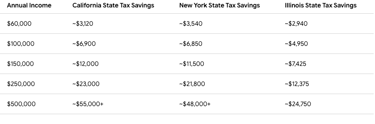

💰 Florida's Tax Advantages: The Numbers Behind the Hype

The "no state income tax" thing is real. Let's quantify it.

What You Save With No State Income Tax

Calculations based on 2026 state marginal income tax rates. Federal taxes apply in all states equally.

This is significant money. For a household earning $150,000 moving from New York to Florida, the state income tax savings alone can cover several months of rent or make a meaningful dent in higher insurance costs.

Other Florida Tax Advantages

No state estate or inheritance tax — Florida repealed its estate tax in 2004

No state tax on Social Security income — retirees, this is for you

No state tax on pension income

Homestead Exemption reduces property tax burden (see Housing section above)

Sales tax: Florida's base state sales tax is 6%, with counties adding 0.5–1.5% (total typically 6.5–7.5%). Groceries and most prescription drugs are exempt.

📊 Florida vs. Other States: Cost of Living Comparison

Here's how Florida stacks up against commonly compared states across key expense categories:

Sources: MIT Living Wage Calculator, Zillow, Insurance Information Institute, EIA, BLS Consumer Price Index, 2026

The takeaway: Florida wins big on income taxes and comes in near-average on groceries and healthcare. It loses ground on homeowners insurance (especially coastal) and auto insurance. Versus California and New York, it's still a strong financial value. Versus Texas or Georgia, it's more of a coin flip — Texas has no income tax either, with lower insurance costs, while Georgia has income tax but much cheaper housing.

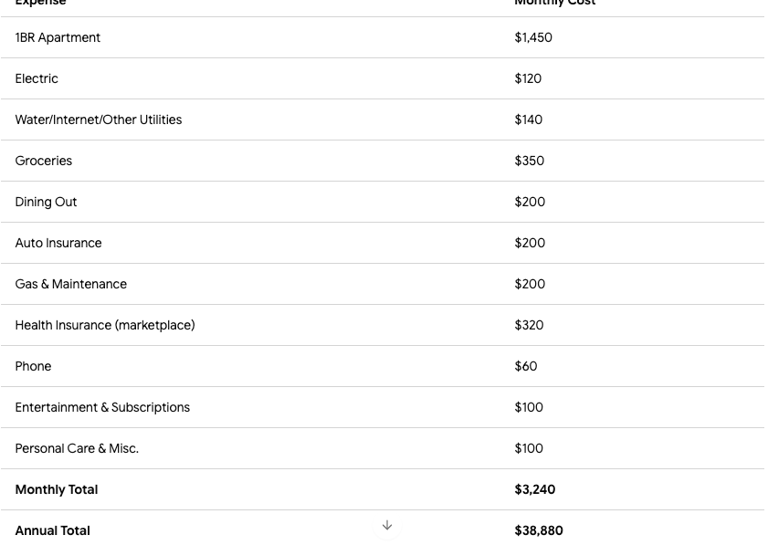

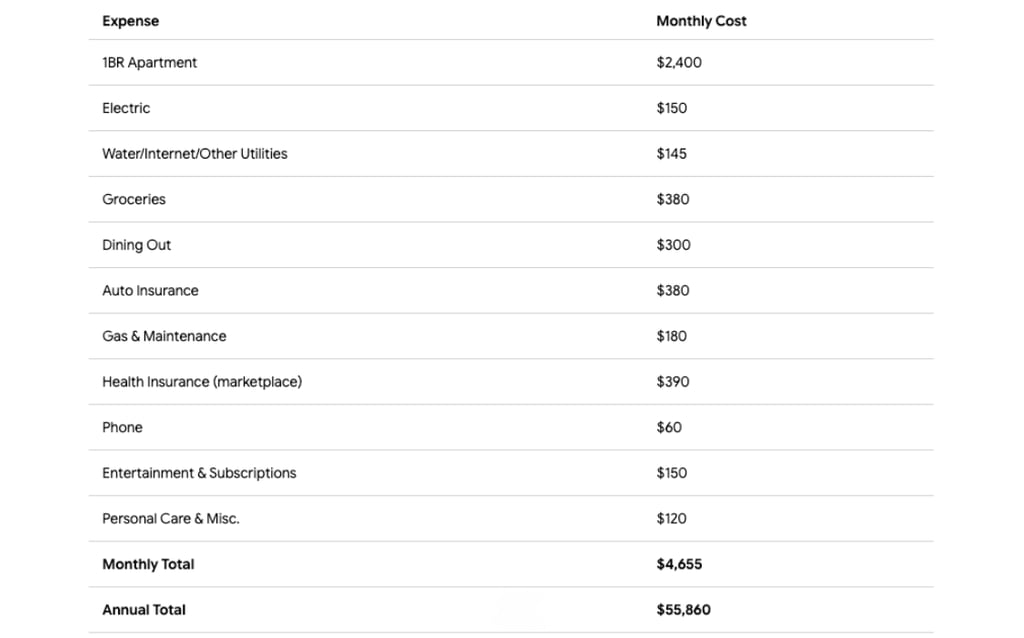

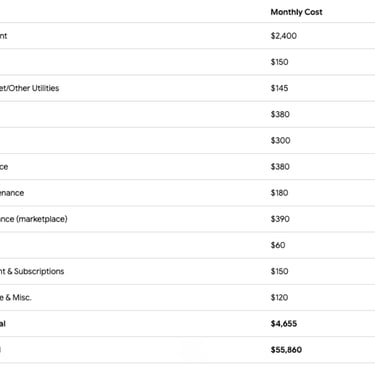

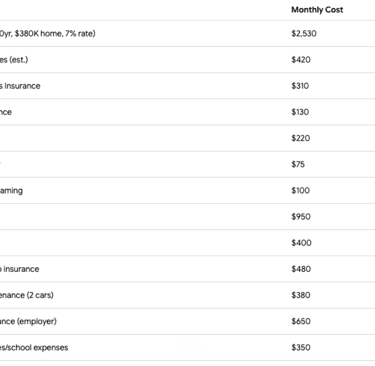

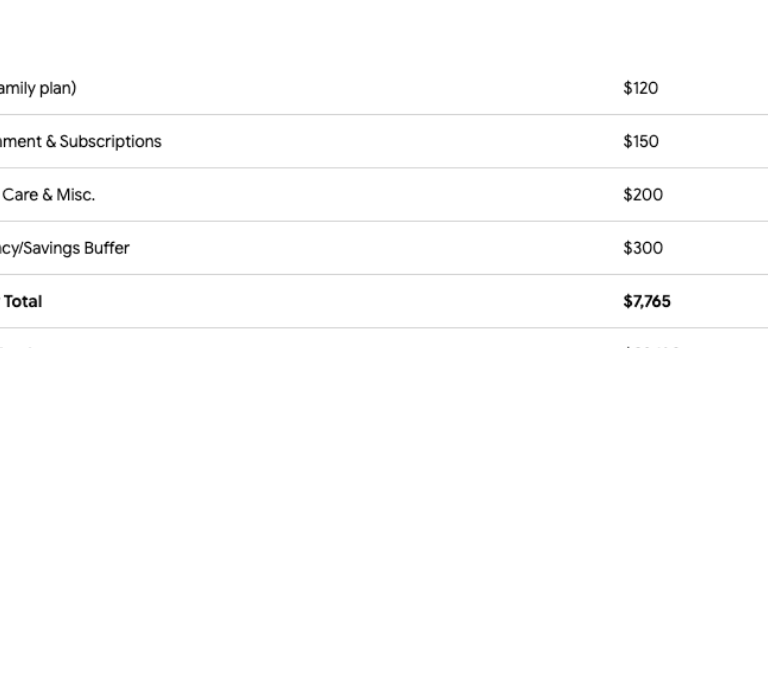

🧾 Sample Monthly Budgets

Budget 1: Single Adult, Renting in Jacksonville

Budget 2: Single Adult, Renting in Miami

Budget 3: Family of Four, Homeowners in Orlando Suburbs

Budget 4: Retired Couple, Homeowners in Sarasota

💡 Smart Ways to Stretch Your Florida Dollar

You didn't come all the way to Florida to be stressed about money. Here's how Floridians make the numbers work:

Housing Hacks

Consider inland: Living 20–30 miles from the coast often means 25–40% lower home prices and dramatically cheaper insurance

Buy in an HOA with included utilities: Some communities bundle water, trash, and cable — compare total costs, not just HOA fees

New construction: Many new-build communities in Florida offer builder incentives including rate buydowns, which can meaningfully lower your monthly mortgage payment

Insurance Strategies

Roof age matters enormously: A roof under 10 years old can save you $800–$2,000/year on homeowners insurance

Wind mitigation inspection: $150–$200 upfront can yield 15–40% in annual premium discounts

Bundle everything: Home, auto, and sometimes umbrella policies bundled with the same carrier typically earn 10–20% multi-policy discounts

Use an independent insurance agent: They can shop multiple carriers simultaneously — a major advantage in Florida's complex insurance marke

Everyday Savings

Publix BOGO sales are a genuine strategy: Buy One Get One deals run weekly and can significantly reduce grocery spend if you plan meals around them

State parks: Florida's 175 state parks are extraordinary — and annual passes are $60 for a family. Beaches, hiking, kayaking, springs — all included

Year-round outdoor living: Floridians genuinely spend less on indoor entertainment because outside is often the best option

Florida Resident discounts: Theme parks (Disney, Universal, SeaWorld, Busch Gardens), attractions, and many restaurants offer Florida resident pricing — often 30–50% below standard admission

❓ Florida Cost of Living FAQ

Q: Is Florida still affordable in 2026? Florida remains more affordable than coastal California, New York, or Massachusetts — particularly when factoring in the tax savings from no state income tax. However, the rapid growth of the past several years has pushed Florida solidly into the "mid-range" category nationally. It's no longer a bargain market, but with smart choices — particularly location within the state — Florida can offer genuine value.

Q: What is the minimum salary to live comfortably in Florida? The MIT Living Wage Calculator estimates a single adult in Florida needs to earn approximately $22–$26/hour ($45,000–$54,000/year) to cover basic living expenses without assistance. A family of four with two working adults needs roughly $26–$30/hour per adult. "Comfortably" — including savings, retirement contributions, and some discretionary spending — typically requires $55,000–$75,000/year for a single adult and $100,000–$130,000/year for a family of four.

Q: What's the cheapest city to live in Florida? Among Florida cities with strong job markets and quality of life, Jacksonville, Gainesville, Tallahassee, Ocala, and Pensacola consistently rank as the most affordable. Smaller inland towns like Lakeland, Deland, and Sebring offer even lower costs but with fewer employment opportunities.

Q: What is the average electric bill in Florida? The average Florida household pays approximately $130–$250/month for electricity, with summer months (July–September) typically running $50–$100 higher than winter months. Electric bills are higher in Florida than the national average due to year-round air conditioning demands.

Q: How much is homeowners insurance in Florida? Florida homeowners pay an average of $3,200–$4,500/year for homeowners insurance statewide — significantly higher than the national average of approximately $1,800/year. South Florida coastal areas can run $5,000–$8,000+ annually. Flood insurance (required in many areas, strongly recommended in all) adds an additional $700–$2,500/year.

Q: Does Florida have property taxes? Yes. Florida property taxes are calculated at the local county level and vary by location. Effective rates typically fall between 0.7% and 1.2% of assessed value. The Homestead Exemption reduces your assessed taxable value by up to $50,000 for your primary residence, and the Save Our Homes cap limits annual assessment increases.

Q: Is it cheaper to live in Florida than Texas? It's close. Both states have no state income tax. Texas generally has lower homeowners insurance and auto insurance rates than Florida, and slightly lower median home prices in many markets. Florida has lower grocery costs on average and a stronger tourism economy that creates diverse employment opportunities. For most families, the two states are relatively comparable — location within each state matters as much as the state itself.

Q: What are the hidden costs of living in Florida? The costs that most surprise Florida newcomers: homeowners insurance (much higher than expected), auto insurance (same), the summer electric bill spike, flood insurance (separate from and not included in standard homeowners policies), hurricane preparedness supplies ($500–$1,500 upfront), HOA fees in many communities, and the general cost increase that comes with living near desirable coastlines.

The Bottom Line on Florida's Cost of Living

Here's the honest Florida Current summary: Florida is a financial trade-off, not a financial miracle.

You gain significantly on income taxes — and that savings is real and substantial. You gain on groceries. You gain on year-round outdoor living that reduces what you spend on entertainment and gym memberships and ski trips.

You pay more than the national average for homeowners insurance, auto insurance, and electricity. You'll need flood insurance if you're near water. And housing, while cheaper than coastal California or New York, isn't the screaming bargain it was five years ago.

What we can tell you from experience is this: the Floridians who thrive financially are the ones who do the math before they move — who compare their current total cost of living (including state taxes) to their projected Florida total cost of living (including insurance and utilities). They factor in the intangibles: January weather, 1,200 miles of coastline, year-round farmers markets, and that particular kind of relaxed warmth that seeps into your bones after your first Florida winter.

For many people — perhaps most — Florida comes out ahead when you run those numbers honestly. But it's the honest version that matters.

We're Florida Current. We're here to give you the real picture, not the postcard version.

Welcome (or welcome back) to the Sunshine State. 🌴

🔗 More from Florida Current:

Best Places to Retire in Florida: A Genuine Guide for Real People Making Real Decisions

The Florida New Resident Checklist: 25 Things to Do After the Moving Truck Leaves

Everyday Life in Florida: What It Actually Feels Like to Live Here

Florida Weather Guide: Month-by-Month Temperatures, Seasons, and What to Expect

Florida Hurricane Season 2026 Explained: A Practical Guide for Residents

Sources: U.S. Bureau of Labor Statistics, Florida Realtors Association, Zillow Research, Apartment List, MIT Living Wage Calculator, Florida Office of Insurance Regulation, Insurance Information Institute, U.S. Energy Information Administration, Florida Department of Revenue, U.S. Census Bureau, Bankrate, Insurify, CoStar Group. Data reflects available figures as of June 2026.

Florida native Luana B. Gann brings more than 30 years of publishing, editing, and journalism experience to Florida Current. With a deep appreciation for the Sunshine State’s culture, lifestyle, and ever-changing landscape, she is dedicated to helping readers discover what’s new, noteworthy, and uniquely Florida.

CONTACT

Reach out for questions or feedback anytime.

contact@FLAcurrent.com

© 2026. All rights reserved.